“My purpose is to empower women in the most impactful area of life – her financial confidence.”

Tracey Sofra

What Drives Me

“For over three decades, I've worked with thousands of women across Australia to grow their financial confidence and their wealth successfully and sustainably”

Tracey Sofra

How You Can Work With Me

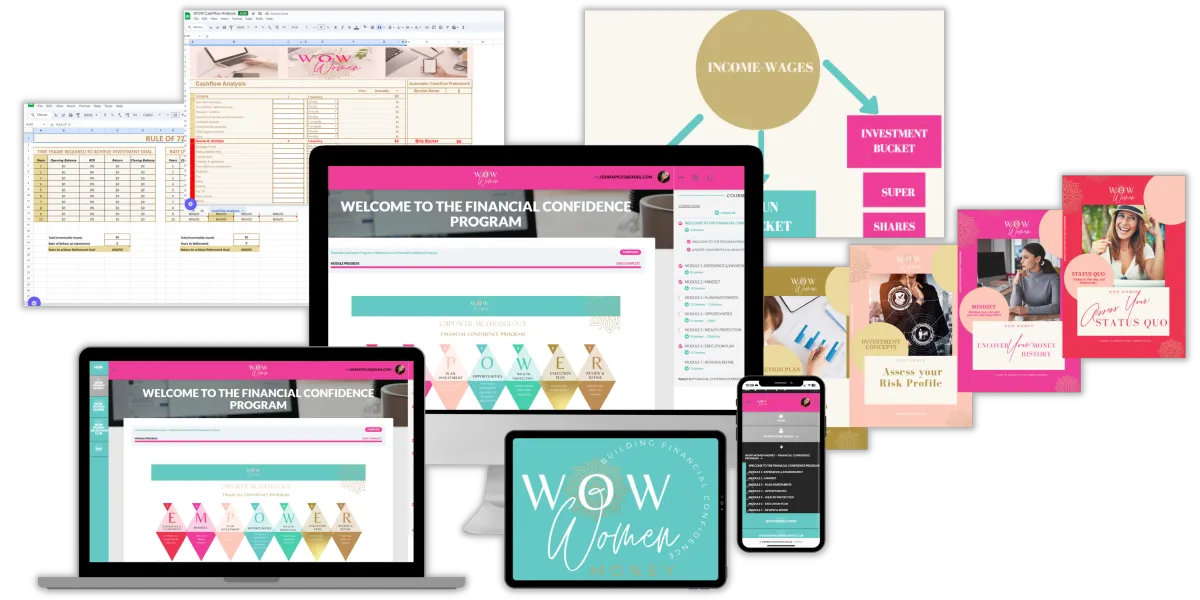

"FINANCIAL CONFIDENCE PROGRAM"

E.M.P.O.W.E.R.

7 Steps to Build your Financial Confidence

These 7 steps are the difference between struggling with money stress and achieving financial success. If

you can imagine a life of choice without worrying about money again, read on - you're in the right place.

Seven enlightening learning modules to help you navigate the path.

Complete with downloadable workbooks. These essential resources provide hands-on

guidance and exercises to boost your financial acumen. Take control of your finances, one

page at a time, and build a solid foundation for lasting financial confidence.

Connect with like-minded individuals, share insights, and access invaluable tools to manage

your finances with precision. Together, we're building a stronger, financially confident

future!

"Tracey's passion around financial confidence is infectious leaving you inspired to challenge the status quo, gain clarity and create change."

"Tracey your invaluable advice has been empowering and profound on so many levels. Thank you for changing my life and giving me the confidence to know I've got this"

"I thought I had a pretty good financial background but I learned so much more from Tracey's expertise and financial knowledge! Now I'm going to put it all into place to get the financial freedom I've always wanted."

© 2026. Tracey Sofra. Investing in women's empowerment. All rights reserved.